#Ambulatory Health Care Services

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

28.6 is the average number of monthly visits per US mobile user.

Text

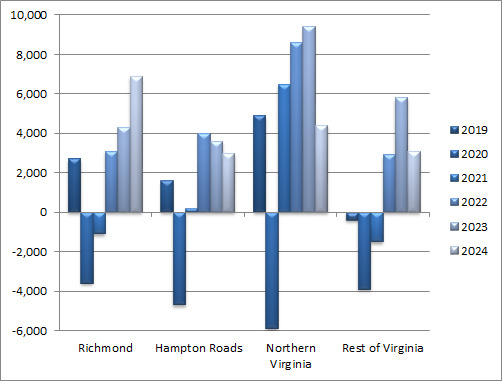

Annual Change in HC&SA Regional Employment (Not Seasonally Adjusted, Full-Year Change for 2019-2023, Year-to-Date Change in 2024)

HWDC Releases December 2024 Health Workforce Brief Series 2: Regional and Sectoral Employment

The Department of Health Professions' Healthcare Workforce Data Center has released the December 2024 issue of its Virginia Health Care Workforce Brief Series 2: Regional and Sectoral Employment. Data in this Brief is not seasonally adjusted.

According to preliminary estimates, every region in Virginia enjoyed positive Health Care & Social Assistance (HC&SA) employment growth in November. This job growth was particularly impressive in Northern Virginia and Richmond. Northern Virginia’s HC&SA sector created 1,800 new jobs in November, a gain that represents a one-month annualized employment growth rate of 14.2%. At the same time, Richmond produced 1,100 new HC&SA jobs in November, which translates into an even faster 14.4% annualized employment growth rate. With this gain, Richmond’s HC&SA sector has now created a total of 5,400 jobs over the past three months. This increase in Richmond’s HC&SA employment represents an impressive three-month annualized growth rate of 25.3%. Richmond is also enjoying strong long-term HC&SA employment growth as well: Over the past 12 months, Richmond’s HC&SA sector has increased employment by 8.5%. Meanwhile, Hampton Roads’ HC&SA sector produced 700 new jobs in November, and the Rest of Virginia increased HC&SA employment by 300 during the month.

Virginia also enjoyed broad-based employment growth across all four HC&SA subsectors in November. This job growth was strongest in Ambulatory Health Care Services, which was responsible for two thirds of Virginia’s total statewide HC&SA employment gain during the month. In November, Ambulatory Health Care Services created 2,700 new jobs, a gain that represents a one-month annualized employment growth rate of 15.7%. With this gain, Ambulatory Health Care Services have now increased employment by a total of 6,300 so far this year. Nursing & Residential Care Facilities also enjoyed double-digit employment growth during the month: In November, this HC&SA subsector produced 700 new jobs across the state, which translates into an 11.2% annualized employment growth rate. Meanwhile, Hospitals enjoyed their tenth consecutive month of positive employment growth after this HC&SA subsector created 400 new jobs in November, which represents a one-month annualized growth rate of 4.2%. Finally, Social Assistance experienced a small employment gain in November with the creation of 100 new jobs during the month.

To access the full brief, click the link above. To see all Virginia Health Care Workforce Briefs and to access archival briefs, visit our website.

#data#employment#growth#health#Richmond#Hampton Roads#Northern Virginia#Social Assistance#Ambulatory Health Care Services#Nursing & Residential Care Facilities#health care economics#health care workforce#health care briefs#Healthcare Workforce Data Center#jobs#statistics#Virginia health care employment#November health care employment

0 notes

Text

What is ambulatory coding?

The process of giving particular number codes to medical diagnoses and treatments carried out in outpatient settings, like clinics, doctor’s offices, and outpatient surgery centers, is known as ambulatory coding. It is critical to understand ambulatory surgery centers (ASC) and their codes. Medical research, health care monitoring, and billing all make use of these codes. They give insurers and healthcare professionals a common language to use when discussing medical services. Ambulatory or outpatient surgery provides same-day surgical care for a variety of procedures.\

#health care#medical coding services#healthcare#medicalcare#photographers on tumblr#ambulatory coding#health and wellness

0 notes

Text

#Ambulatory Health Care Services Market#Ambulatory Health Care Services Market scope#Ambulatory Health Care Services Market size#Ambulatory Health Care Services Market share#Ambulatory Health Care Services Market trend#Ambulatory Health Care Services Market analysis

0 notes

Text

Conclusion

Medical institutions are a reflection of the cisnorm — and not only because ambulatory clinics demand that our performances conform to cisgender molds, but also because all spaces that are not specifically designated for trans people are veiled as being designated for cis people, with racial, class and various bodily segregations. Trans clinics are not exempt from this. The people who apply for the transsexualization processes and usually undergo the various stages of evaluation, as Bento has shown, are those who, to some extent, fit into a cisgender social reading, or — truthfully or not — claim to desire it. Medical authorities do not give up their place as authorities. The institutional walls continue to protect the determinations of what is or is not ‘being trans’, of how we should or should not be treated, of what access we can or cannot have. The annihilation of trans subjectivities falls under the concept of epistemicide, insofar as any possibility of self-determination and knowledge production about transsexuality by trans people is annulled.

Since the early 2000s, with the insurgence of trans social movements in Brazil — such as the National Association of Travestis and Transsexuals (ANTRA) or the Brazilian Institute of Transmasculinities (IBRAT) -, popular pressure on pathologization has been strong, but only achieved results by the end of the first decade. The ICD-11 and DSM-V have modified its sections on transsexuality. However, they continue to catalog trans identities as something-not-quite-right, whereas cisgenderity remains unnamed. We still depend on medical approval to access surgery and hormone therapy. The authority of “scientific opinion” remains, even after changes to the ICD and DSM. This shows us how institutions operate: not without authority, not without hierarchy, not without a clear dynamic of subjection.

The government-regulated trans clinics express the materialization of cisgender norm. The means by which we can access health care are the same ones that force us into a violent normativity. And these are the same forces that compel us to introject cisnormative trans subjectivities, based on the dynamics of culpability and segregation (GUATTARI; ROLNIK, 1996). In general terms, there is no possibility of social emancipation that passes through institutional hands, whether it be the government’s so-called ‘assistance’ of dissident people, affirmative policies aimed at marginalized groups, or the provision of minimal services that seek to protect trans people from violence. The monoculture of knowledge (SANTOS, 2014) is a constant that underpins different institutionalized spaces. Even though these ambulatory policies and institutional initiatives of “care” can be fruitful, it cannot be denied that every institutional apparatus, once it represents the arms of the State, operates to maintain segregation. The “care” provided by trans clinics translates into epistemic violence, the erasure of subjectivities and the imposition of the cisnorm. The name change protocols offered by registry offices and the judicial system cause embarrassment, inaccessibility and vexatious situations.

One cannot fight for freedom except from it and using it as the main instrument (BAKUNIN, 2021); one cannot defend the emancipation of dissident bodies through institutions, as this would be the same as striving for freedom by means of the very same instruments that produce imprisonment. Only through libertarian means — that stand against the authoritarianism of institutionalized scientific knowledge — can we glimpse emancipation.

#queer#queer theory#cisheteropatriarchy#tranarchism#transgender#transgender liberation#cisnormativity#decoloniality#decolonization#institutional violence#transsexuality#anarchism#anarchy#anarchist society#practical anarchy#practical anarchism#resistance#autonomy#revolution#communism#anti capitalist#anti capitalism#late stage capitalism#daily posts#libraries#leftism#social issues#anarchy works#anarchist library#survival

6 notes

·

View notes

Text

Health in Italy

I realized I had written a quarantine vocabulary and probably never posted it? But honestly, I turned it into somethng else that may be interesting for you. It’s a very fast and not too deepened post about how health works in Itlaya, but hopefully it’s gonna give you an idea. In case you need. Ofc, here I am if I had forgotten something (which probably I have).

Il medico di base = the general pratictioner

Each of us has a doctor (usually the same person for the same family members, but not necessarily: it depends on how many free places they have cause each of them only have a maximum amount of people they can take care of) that is payed by the State (by the mutua = National health service; in fact they were called “medico della mutua” too) to which we can go anytime we feel sick or need something (even prescriptions for other exams or just a paper to be able to join the gym -that states we’re fine; or a paper that states we cannot go to work cause we’re sick and for how many days: this only if we work into public structures not if we work by ourselves ofc). This doctor works for a specific amount of hours each day (Monday-Friday), but they may visit you at home if you can’t go to their ambulatory/office. If it’s holiday or pre-holiday, you may call the “Guardia Medica”, in which there are other doctors that can visit you either in their ambulatory or at home for emergencies, but you better pray they answer you or you better go to the hospital’s first aid/emergency room.

Il dottore = the doctor; in Italy it should be “il medico” cause everyone who’s graduated from University is a “dottore” or “dottoressa”. “dottore” = “medico” is more of a slang but we do use it anyway.

We either have public health, so we can go to the hospital for exams, most of which are payed (sometimes entirely, sometimes only by half, other times at all but they don’t cost much -it depends also by age and general situation of the patient) by the State. Same goes for some medicines that are free cause are payed by the State (some others are payed partially, others ofc not at all: it depends what they serve for and who needs to take them).

But we also have private health: doctors have their own ambulatories/offices where they can visit you. Sometimes they work in private clinics too. These type of visits may cost a bit more but are way faster than the ones you can programme in hospitals (it may take you months to years for a visit atm, even serious ones). And if you have any external support as any other “mutua” (health insurances that may be private too/belong to associations you may join if you have a job or as a family member, and you pay every year for) or insurances that is not just the National one, you can get some of your money back or a discount even in private clinics. Some insurances may pay your hospital recovery or surgeries too.

#parole words#vocabs#vocabulary#italian vocabulary#italian vocabs#langblr#language#italian language#italian langblr#health vocabs#it#italian#languages#italianblr#italiano#lingua italiana

25 notes

·

View notes

Text

I think if there is something that I've learned this year having to deal with a lot of healthcare nonsense it's that many patients (myself included) need to learn our rights, and that there ARE options that we can take when we can't afford payment for drugs or care and when we get rejected by insurance for coverage for something. I wish to god we had a better healthcare system in this country; I do, but for now we have to live with the bullshit we have, and I think people would be served better by getting educated about their options and rights in the now to reduce harm in the now, while we fight for a better system. For now, here are some things that are of interest:

If you do not have health insurance at this time, you can get it through healthcare.gov. It doesn't matter where in the country you live, what your previous claims payment history is or what your current medical conditions are. You can pay for and get ANY plan that is offered on this site. This is defined through ACA Subtitle D, Part I.

When you look at the plans not signed in, they look SUPER expensive. They are not. Create an account and submit your tax information. Once your previous year's tax information is submitted, the site will tell you what your tax-credit reduction is for your monthly premiums. This is the amount of $ that the government will subsidize your premiums for. The less money you make, the more this amount will be. If your income was greater last year than it is this year, when you file your taxes you will get money back that you should have received in reductions on your premiums. If your income is greater, you owe. They give you the choice of how much of the credit to take in the now. If you choose not to use all of it, you get the unused amount back on your taxes.

If you have marketplace plan questions, call the healthcare dot gov help line (1-800-318-2596) and someone will help you. They will answer any questions you have, no matter how dumb they are. You can ask them simple stuff like "What is a premium?" and they helpfully explain it.

No insurance company can raise your premiums based on your claims payment history, your health conditions, your health history or any other form of "evidence of insurability". They cannot deny you a plan for any of these reasons or deny you renewal of a plan for them. You have rights, if your insurance is trying to do this, you can report them to the government. It is illegal for them to discriminate against YOU for any of these reasons. This is all defined either under ACA Subpart I: General Reform, sect 2702, sec 2703, and section 2705.

If you are over 65, you are eligible for medicare, and you should get it. If you have a serious disability, you can get medicare earlier. This will significantly reduce your healthcare costs. You have already paid into it if you have been paying taxes on a W2.

If you are poor, you may qualify for medicaid. If you are unemployed you probably qualify for medicaid. Eligibility requirements vary by state, but if you are below the federal poverty line and under 65, you are almost certainly eligible. Medicaid is low cost and covers most services. If you have children and are poor, you can get CHIP.

Certain services are considered "Essential Health Benefits" under the ACA and ALL plans are required to cover them. These EHBs include items and services in the following ten benefit categories: (1) ambulatory patient services; (2) emergency services; (3) hospitalization; (4) maternity and newborn care; (5) mental health and substance use disorder services including behavioral health treatment; (6) prescription drugs; (7) rehabilitative and habilitative services and devices; (8) laboratory services; (9) preventive and wellness services and chronic disease management; and (10) pediatric services, including oral and vision care. If you plan refuses to provide ANY coverage for items and services under these categories, that is illegal and you can report them.

If you visit a non-for-profit hospital for emergency services, and are uninsured or poor, they must provide you with financial assistance, whether that is FREE care or significantly reduced care. This applies even for insured patients who are visiting an emergency room that is not in their network. Talk to their billing department and ask about financial assistance and charity care.

Under the No-Surprises Act, a subsection of the CAA 2021, a provider of emergency services cannot balance bill you (bill you money after you have paid your deductible, copay, coinsurance and your insurance pays out their obligation to make up for costs on the visit from their providers being not in your network). This is something new I didn't know about until my current situation lol.

Certain forms of medical debt CANNOT be reported on your credit report. Additionally, if you apply for an FHA mortgage to purchase a home, the FHA does not consider medical debt when assessing mortgage eligibility. For more information about new rules regarding medical debt as related to creditworthiness here is the general bulletin.

If you are denied coverage for a medically necessary drug or service, you have the right to appeal this. Call your insurance company and ask for an explanation for the denial of coverage. Sometimes, your doctor can provide a letter of medical necessity for the service to get you coverage. The same drugs and services can be billed under different classifications, which may affect coverage. Read through your plans benefits booklet to find if the service you are being denied is covered under a different billing classification (usually called a CPT #). If this is the case, you can work with your provider to reclassify the billing of the drug or service to get coverage. Arm yourself with all the right vocabulary and information by reading through your plan's benefits booklet and by requesting an extended EOB (explanation of benefits) for the claim in question. Note that you cannot get extended EOBs for medication claims, but you can for services. You may also want to enlist your provider in your fight against charges as there is certain information that they can more easily access than you can and that they can do on your behalf.

Many drugs have manufacturer coupons that you can use to reduce your copay. These coupons can be applied WITH your insurance. If a pharmacy employee tells you otherwise, they don't know what the fuck they're talking about. Ask to speak with the head pharmacist about this. You can find many kinds of drug coupons through sites like goodrx or the manufacturer of your drug's website. Sometimes your doctor may also have coupons; ask them. If you have an especially competent pharmacist, they can also help you find coupons or discounts.

Anyhow, I hope someone finds this helpful. Learn your rights and your terminology so that you can get the care you need and deserve!

#healthcare#know your rights#insurance#health insurance#reference#resources#medical care#issues#ref#long post for ts

5 notes

·

View notes

Text

Urology Medical Device Market Trends, Share, Opportunities and Forecast By 2029

The Urology Medical Device Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2029. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers. Through the use of SWOT and PESTEL analyses, it evaluates the sector’s strengths, weaknesses, opportunities, and threats, while considering political, economic, social, technological, environmental, and legal influences. Expert evaluations of competitor strategies and recent developments shed light on geographical trends and forecast the market’s future direction, creating a solid framework for strategic planning and investment decisions.

Brief Overview of the Urology Medical Device Market:

The global Urology Medical Device Market is expected to experience substantial growth between 2024 and 2031. Starting from a steady growth rate in 2023, the market is anticipated to accelerate due to increasing strategic initiatives by key market players throughout the forecast period.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-urology-medical-device-market

Which are the top companies operating in the Urology Medical Device Market?

The report profiles noticeable organizations working in the water purifier showcase and the triumphant methodologies received by them. It likewise reveals insights about the share held by each organization and their contribution to the market's extension. This Global Urology Medical Device Market report provides the information of the Top Companies in Urology Medical Device Market in the market their business strategy, financial situation etc.

Medtronic, Siemens, Abbott, GENERAL ELECTRIC, BD, Stryker, Boston Scientific Corporation, Cardinal Health, Intuitive Surgical, Cook, Olympus Corporation, Johnson & Johnson Private Limited ., Fresenius Medical Care AG & Co. KGaA, Baxter, Richard Wolf GmbH, Dornier MedTech., KARL STORZ SE & Co. KG, Endo Pharmaceuticals Inc., HealthTronics Inc., MEDI TECH DEVICES PVT LTD, and Coloplast Corp

Report Scope and Market Segmentation

Which are the driving factors of the Urology Medical Device Market?

The driving factors of the Urology Medical Device Market are multifaceted and crucial for its growth and development. Technological advancements play a significant role by enhancing product efficiency, reducing costs, and introducing innovative features that cater to evolving consumer demands. Rising consumer interest and demand for keyword-related products and services further fuel market expansion. Favorable economic conditions, including increased disposable incomes, enable higher consumer spending, which benefits the market. Supportive regulatory environments, with policies that provide incentives and subsidies, also encourage growth, while globalization opens new opportunities by expanding market reach and international trade.

Urology Medical Device Market - Competitive and Segmentation Analysis:

**Segments**

- Based on product type, the urology medical device market can be segmented into dialysis equipment, endoscopes, lithotripters, stents, urodynamic equipment, and others. The endoscopes segment is anticipated to witness significant growth during the forecast period due to the increasing adoption of minimally invasive procedures in urology. - By application, the market can be categorized into benign prostatic hyperplasia, kidney diseases, urinary stones, urinary incontinence, and others. The urinary stones segment is expected to show substantial growth, driven by the rising prevalence of kidney stones globally. - On the basis of end-user, the market is divided into hospitals, clinics, ambulatory surgical centers, and others. The hospital segment is likely to dominate the market owing to the high patient footfall and availability of advanced medical infrastructure.

**Market Players**

- Boston Scientific Corporation - Olympus Corporation - Stryker - Cook Medical - Coloplast Group - KARL STORZ SE & Co. KG - ROCAMED - Richard Wolf GmbH - Medtronic - Teleflex Incorporated - Baxter - Fresenius Medical Care AG & Co. KGaA

These key market players are focusing on strategic initiatives such as product launches, collaborations, and acquisitions to strengthen their market presence and expand their product offerings. The competition in the urology medical device market is intense, leading companies to invest in research and development activities to bring innovative solutions to the market. The increasing prevalence of urological disorders, coupled with the growing geriatric population, is expected to drive market growth in the coming years.

The global urology medical device market is projected to witness significant growth during the forecast period. Factors such as the increasing incidence of urological disorders, technological advancements in medical devices, and the growing awareness about urological treatments are contributing to market expansion. North America is expected to hold a substantial marketThe global urology medical device market is poised for substantial growth in the upcoming years, driven by several key factors. The segmentation of the market into various product types such as dialysis equipment, endoscopes, lithotripters, stents, urodynamic equipment, and others allows for a comprehensive understanding of the market landscape. The endoscopes segment is expected to experience significant growth due to the rising adoption of minimally invasive procedures in urology, which offer benefits such as faster recovery times and reduced post-operative complications. The increasing prevalence of urinary stones globally is set to boost the demand for urology medical devices, particularly in the urinary stones segment.

In terms of application segmentation, categories like benign prostatic hyperplasia, kidney diseases, urinary stones, and urinary incontinence play a crucial role in shaping market dynamics. The urinary stones segment is projected to exhibit notable growth owing to the escalating incidence of kidney stones worldwide. This growth can be attributed to factors such as dietary habits, lifestyle changes, and genetic predispositions that contribute to the development of urinary stones. As a result, market players are likely to focus on developing innovative devices and technologies to address the specific needs of patients with urinary stones, thereby driving market expansion in this segment.

Moreover, the segmentation based on end-users, including hospitals, clinics, ambulatory surgical centers, and others, provides insights into the distribution channels and preferences of healthcare providers. The dominance of the hospital segment in the urology medical device market can be attributed to the high patient volume and the presence of advanced medical infrastructure in hospital settings. Hospitals often serve as primary points of care for patients with urological disorders, leading to a substantial market share for this segment. Additionally, the increasing adoption of advanced medical technologies and the emphasis on providing comprehensive urological care are expected to further bolster the demand for urology medical devices in hospital settings.

Overall, the competitive landscape of the urology medical device market is characterized by the**Market Players:**

- Medtronic - Siemens - Abbott - GENERAL ELECTRIC - BD - Stryker - Boston Scientific Corporation - Cardinal Health - Intuitive Surgical - Cook - Olympus Corporation - Johnson & Johnson Private Limited - Fresenius Medical Care AG & Co. KGaA - Baxter - Richard Wolf GmbH - Dornier MedTech - KARL STORZ SE & Co. KG - Endo Pharmaceuticals Inc. - HealthTronics Inc. - MEDI TECH DEVICES PVT LTD - Coloplast Corp

The urology medical device market is experiencing significant growth and is poised for further expansion in the forthcoming years. Multiple factors are driving this growth, including the increasing incidence of urological disorders, advancements in medical device technologies, and a raised awareness regarding urological treatment options. The market segmentation into various product types, such as dialysis equipment, endoscopes, lithotripters, stents, urodynamic equipment, and others, provides a comprehensive overview of the diverse landscape within the industry. Specifically, the endoscopes segment is expected to witness substantial growth due to the rising preference for minimally invasive procedures in urology, which offer benefits like faster recovery times and reduced post-operative complications.

Furthermore, the application segmentation of the market into categories like benign prostatic hyperplasia, kidney diseases, urinary stones, and urinary incontinence

North America, particularly the United States, will continue to exert significant influence that cannot be overlooked. Any shifts in the United States could impact the development trajectory of the Urology Medical Device Market. The North American market is poised for substantial growth over the forecast period. The region benefits from widespread adoption of advanced technologies and the presence of major industry players, creating abundant growth opportunities.

Similarly, Europe plays a crucial role in the global Urology Medical Device Market, expected to exhibit impressive growth in CAGR from 2024 to 2029.

Explore Further Details about This Research Urology Medical Device Market Report https://www.databridgemarketresearch.com/reports/global-urology-medical-device-market

Key Benefits for Industry Participants and Stakeholders: –

Industry drivers, trends, restraints, and opportunities are covered in the study.

Neutral perspective on the Urology Medical Device Market scenario

Recent industry growth and new developments

Competitive landscape and strategies of key companies

The Historical, current, and estimated Urology Medical Device Market size in terms of value and size

In-depth, comprehensive analysis and forecasting of the Urology Medical Device Market

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2024-2031) of the following regions are covered in Chapters

The countries covered in the Urology Medical Device Market report are U.S., Canada and Mexico in North America, Brazil, Argentina and Rest of South America as part of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe in Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA

Detailed TOC of Urology Medical Device Market Insights and Forecast to 2029

Part 01: Executive Summary

Part 02: Scope Of The Report

Part 03: Research Methodology

Part 04: Urology Medical Device Market Landscape

Part 05: Pipeline Analysis

Part 06: Urology Medical Device Market Sizing

Part 07: Five Forces Analysis

Part 08: Urology Medical Device Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers And Challenges

Part 13: Urology Medical Device Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse More Reports:

Japan: https://www.databridgemarketresearch.com/jp/reports/global-urology-medical-device-market

China: https://www.databridgemarketresearch.com/zh/reports/global-urology-medical-device-market

Arabic: https://www.databridgemarketresearch.com/ar/reports/global-urology-medical-device-market

Portuguese: https://www.databridgemarketresearch.com/pt/reports/global-urology-medical-device-market

German: https://www.databridgemarketresearch.com/de/reports/global-urology-medical-device-market

French: https://www.databridgemarketresearch.com/fr/reports/global-urology-medical-device-market

Spanish: https://www.databridgemarketresearch.com/es/reports/global-urology-medical-device-market

Korean: https://www.databridgemarketresearch.com/ko/reports/global-urology-medical-device-market

Russian: https://www.databridgemarketresearch.com/ru/reports/global-urology-medical-device-market

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 1333

Email:- [email protected]

#Urology Medical Device Market Size#Urology Medical Device Market Shares#Urology Medical Device Market Forecast#Urology Medical Device Market Growth#Urology Medical Device Market Demand

0 notes

Text

Intubation Tubes Market: $3.9B in 2023 to $7.2B by 2033, 6.1% CAGR

Intubation Tubes Market is centered on the production and distribution of medical devices essential for airway management during surgical procedures and in critical care settings. This market includes endotracheal tubes, tracheostomy tubes, and specialized variants, serving hospitals, clinics, and emergency services. Driven by innovations in materials and design, coupled with an increase in surgical procedures and respiratory disorders, the market emphasizes patient safety and comfort.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS25900 &utm_source=SnehaPatil&utm_medium=Article

The market is experiencing significant growth due to advancements in medical technology and the rise in surgical interventions. Orotracheal intubation tubes lead the market because of their extensive use in emergency and elective surgeries. Nasotracheal intubation tubes are the second-largest segment, gaining popularity in specialized surgical procedures and pediatric care. Additionally, reinforced intubation tubes are becoming more common in complex surgeries requiring prolonged intubation.

North America dominates the market, thanks to its advanced healthcare infrastructure and the high prevalence of respiratory disorders. Europe follows closely, with a strong emphasis on healthcare innovation and increasing surgical procedures. In the Asia-Pacific region, countries like China and India are top performers, driven by rising healthcare expenditures and expanding medical tourism. The region’s growing geriatric population and increased awareness about advanced medical procedures further fuel market growth.

Market Segmentation

Type: Orotracheal Intubation Tubes, Nasotracheal Intubation Tubes

Product: Standard Tubes, Reinforced Tubes, Preformed Tubes, Laser Resistant Tubes

Material Type: Polyvinyl Chloride (PVC), Silicone, Polyurethane

Application: Emergency Treatment, Anesthesia, Critical Care

End User: Hospitals, Ambulatory Surgical Centers, Specialty Clinics

Technology: Fibre Optic, Video Laryngoscopy

Device: Reusable, Disposable

Functionality: Cuffed, Uncuffed

Installation Type: Manual, Automated

Mode: Single Use, Multi-Use

In 2023, the market reported approximately 320 million units, with expectations to reach 480 million units by 2033. Orotracheal intubation dominates with a 45% share, followed by nasotracheal intubation at 30%, and other types at 25%. Key players like Medtronic, Teleflex Incorporated, and Smiths Medical hold significant positions through technological advancements and strategic partnerships.

The competitive landscape is influenced by firms’ innovation capabilities and market expansion strategies. Regulatory bodies like the FDA and EMA set stringent standards, impacting product approvals. The market is projected to grow at a 7% annual rate, supported by rising healthcare expenditure and an aging population. Challenges such as regulatory compliance and pricing pressures persist, but innovations in material science and digital health technologies are expected to open new growth opportunities.

Geographical Overview

North America leads, driven by a robust healthcare system and frequent surgical procedures. Europe benefits from a strong healthcare framework and an aging population, with countries like Germany, France, and the UK contributing significantly. Asia-Pacific experiences rapid growth, especially in China and India, due to expanding healthcare sectors and government initiatives. Latin America and the Middle East & Africa offer moderate growth, with notable contributions from Brazil, Mexico, and increased healthcare expenditure in these regions.

#IntubationTubes #AirwayManagement #MedicalDevices #SurgicalCare #RespiratoryDisorders #HealthcareInnovation #PatientSafety #CriticalCare #EndotrachealTubes #Medtronic #Teleflex #SmithsMedical #OrotrachealIntubation #HealthcareGrowth #MedicalTechnology

0 notes

Text

Affordable and Trusted Ambulatory Surgery Center in Brookfield

Looking for a reliable Ambulatory Surgery Center in Brookfield? Our state-of-the-art facility provides expert care for a wide range of same-day surgical procedures, including orthopedic, ENT, and minor cosmetic surgeries. Designed for your comfort and convenience, we ensure shorter wait times, affordable pricing, and exceptional outcomes. With a skilled team of surgeons and modern medical technology, we prioritize your safety and recovery. Experience high-quality care close to home without the hassle of a hospital stay. Visit us today for safe and efficient surgical solutions tailored to your needs!

1 note

·

View note

Text

TAVI Expert in Jaipur Dr. Amit Gupta, Cardiologist and Heart Specialist

Transcatheter Aortic Valve Implantation (TAVI) has revolutionized the treatment of aortic valve stenosis, offering a minimally invasive alternative to traditional open-heart surgery. In Jaipur, Dr. Amit Gupta stands out as a leading expert in this field, bringing over a decade of experience in interventional cardiology.

Understanding TAVI

TAVI is a procedure designed to replace a narrowed aortic valve that fails to open properly, a condition known as aortic stenosis. Unlike conventional valve replacement surgery, TAVI is performed through a catheter inserted into a blood vessel, typically in the leg or chest, guiding a new valve into place without the need for open-heart surgery. This approach is particularly beneficial for patients at high surgical risk.

Dr. Amit Gupta: A Pioneer in TAVI

Dr. Amit Gupta is a distinguished interventional Cardiologist in Jaipur, currently serving as an Additional Director in the Cardiology Department at CK Birla Hospital. His medical journey includes a DM in Cardiology from G. B. Pant Hospital, Delhi, and a fellowship with the Society for Cardiovascular Angiography and Interventions (SCAI) in the USA. With over ten years of experience, Dr. Gupta has honed his skills in various aspects of interventional cardiology, with a special focus on TAVI.

Dr. Gupta's expertise in TAVI is backed by extensive training at prestigious centers across the globe, including London (UK), Milan (Italy), and Stockholm (Sweden). He has also collaborated with renowned cardiologists like Dr. Praveen Chandra at Medanta Hospital, Gurgaon, contributing to over 200 TAVI procedures in India.

Comprehensive Cardiac Care

Dr. Gupta offers a wide range of cardiac services at Safe Heart Clinic and CK Birla Hospital in Jaipur. His expertise encompasses complex coronary stent interventions, non-surgical device closure of heart defects (such as ASD, VSD, PDA), MitraClip surgery, and the implantation of cardiac electrical devices like pacemakers and ICDs. He is also proficient in advanced visualization techniques, including Intravascular Ultrasound (IVUS) and Optical Coherence Tomography (OCT) guided coronary stenting. Heart clinic in jaipur

Patient-Centric Approach

Dr. Gupta's practice is characterized by approach, emphasizing personalized care tailored to individual needs. He is known for his compassionate demeanor and commitment to patient education, ensuring that individuals are well-informed about their conditions and treatment options. This dedication has earned him high praise from patients, with testimonials highlighting his kindness, knowledge, and the positive outcomes of his treatments.

State-of-the-Art Facilities

Safe Heart Clinic, under Dr. Gupta's leadership, is equipped with advanced diagnostic and therapeutic technologies. The clinic offers services such as Treadmill Test (TMT), Electrocardiography (ECG), angiography, 2D echocardiography, Holter monitoring, ambulatory blood pressure monitoring, and sleep studies. These facilities enable comprehensive evaluation and management of various cardiac conditions, ensuring patients receive the highest standard of care.

Recognition and Testimonials

Dr. Amit Gupta's extensive experience, advanced training, and patient-focused approach make him a leading TAVI expert and Heart Specialist in jaipur. His commitment to adopting innovative techniques and providing comprehensive cardiac care ensures that patients receive the best possible outcomes.Whether it's performing complex interventions or guiding patients through lifestyle modifications, Dr. Gupta's dedication to heart health is evident in every aspect of his practice.

Dr. Gupta's contributions to cardiology have been recognized by both peers and patients. Testimonials reflect his expertise and compassionate care. For instance, a patient named Kapil Sharma expressed gratitude, stating, "Dr. Amit Gupta is a well-known cardiologist in Jaipur. He is very kind and helpful. Immense knowledge. My mother had some heart-related problems. I visited many doctors, but after meeting Dr. Amit, my search ended at Safe Heart. I am so thankful to Team Safe Heart and Dr. Amit Gupta and will surely recommend them."

Safe Heart Clinic Jaipur is a leading cardiac care center offering exceptional cardiology services in Jaipur, Rajasthan. While the city boasts numerous experienced cardiologists, Safe Heart Clinic stands out for its unmatched excellence in the field of cardiology. Our clinic serves as a beacon of hope for individuals grappling with cardiovascular ailments.

0 notes

Text

Annual Change in HC&SA Subsector Employment (Not Seasonally Adjusted, Full-Year Change for 2019-2023, Year-to-Date Change in 2024)

HWDC Releases November 2024 Health Workforce Brief Series 2: Regional and Sectoral Employment

The Department of Health Professions' Healthcare Workforce Data Center has released the November 2024 issue of its Virginia Health Care Workforce Brief Series 2: Regional and Sectoral Employment. Data in this Brief is not seasonally adjusted.

According to preliminary estimates, both Northern Virginia and the Rest of Virginia enjoyed double-digit Health Care & Social Assistance (HC&SA) employment growth in October. Among Virginia’s four regions, Northern Virginia produced the largest HC&SA employment gain during the month. In October, Northern Virginia’s HC&SA sector created 1,400 new jobs, a gain that represents a one-month annualized employment growth rate of 10.9%. At the same time, the Rest of Virginia added 1,300 new HC&SA jobs to the state’s economy, which translates into an even faster 11.4% annualized employment growth rate. The Rest of Virginia has also enjoyed the fastest long-term job growth in the state thanks to its current 12-month employment growth rate of 4.4%. In fact, the Rest of Virginia has been responsible for nearly 40% of all HC&SA jobs that have been created across the state over the past 12 months. Hampton Roads also enjoyed solid HC&SA employment growth in October with the creation of 500 new jobs during the month, which translates into a 6.0% annualized employment growth rate. However, Richmond’s HC&SA sector saw employment fall by 200 during the month.

Ambulatory Health Care Services created 4,000 new jobs across the state in October, a gain that represents an impressive one-month annualized employment growth rate of 24.6%. Furthermore, this also represents the largest monthly employment gain in Ambulatory Health Care Services in more than four years. Meanwhile, Hospitals enjoyed their ninth consecutive month of positive employment growth after producing 300 new jobs in October. This job gain translates into a 3.1% annualized employment growth rate. At the same time, Social Assistance added 200 new jobs in October, which represents a one-month annualized employment growth rate of 2.7%. Social Assistance and Hospitals are currently the two HC&SA subsectors in the state that are enjoying long-term employment growth that exceeds the overall statewide HC&SA average. Over the past 12 months, Social Assistance has increased employment by 8.0%, while Hospitals have created jobs at a 4.3% rate. As for Nursing & Residential Care Facilities, this HC&SA subsector experienced its first decline in employment since April after losing 1,500 jobs in October. Despite this decline in employment, Nursing & Residential Care Facilities have still created a total of 1,200 jobs so far this year.

To access the full brief, click the link above. To see all Virginia Health Care Workforce Briefs and to access archival briefs, visit our website.

#data#employment#growth#health#Richmond#Hampton Roads#Northern Virginia#Social Assistance#Ambulatory Health Care Services#Nursing & Residential Care Facilities#health care economics#health care workforce#health care briefs#Healthcare Workforce Data Center#jobs#statistics#Virginia health care employment#October health care employment

0 notes

Text

Topics: health care, monopoly

In a recent article for Tikkun, Dr. Arnold Relman argued that the versions of health care reform currently proposed by “progressives” all primarily involve financing health care and expanding coverage to the uninsured rather than addressing the way current models of service delivery make it so expensive. Editing out all the pro forma tut-tutting of “private markets,” the substance that’s left is considerable:

What are those inflationary forces? . . . [M]ost important among them are the incentives in the payment and organization of medical care that cause physicians, hospitals and other medical care facilities to focus at least as much on income and profit as on meeting the needs of patients. . . . The incentives in such a system reward and stimulate the delivery of more services. That is why medical expenditures in the U.S. are so much higher than in any other country, and are rising more rapidly. . . . Physicians, who supply the services, control most of the decisions to use medical resources. . . . The economic incentives in the medical market are attracting the great majority of physicians into specialty practice, and these incentives, combined with the continued introduction of new and more expensive technology, are a major factor in causing inflation of medical expenditures. Physicians and ambulatory care and diagnostic facilities are largely paid on a piecework basis for each item of service provided.

As a health care worker, I have personally witnessed this kind of mutual log-rolling between specialists and the never-ending addition of tests to the bill without any explanation to the patient. The patient simply lies in bed and watches an endless parade of unknown doctors poking their heads in the door for a microsecond, along with an endless series of lab techs drawing body fluids for one test after another that’s “been ordered,” with no further explanation. The post-discharge avalanche of bills includes duns from two or three dozen doctors, most of whom the patient couldn’t pick out of a police lineup. It’s the same kind of quid pro quo that takes place in academia, with professors assigning each other’s (extremely expensive and copyrighted) texts and systematically citing each other’s works in order to game their stats in the Social Sciences Citation Index. (I was also a grad assistant once.) You might also consider Dilbert creator Scott Adams’s account of what happens when you pay programmers for the number of bugs they fix.

One solution to this particular problem is to have a one-to-one relationship between the patient and a general practitioner on retainer. That’s how the old “lodge practice” worked. (See David Beito’s “Lodge Doctors and the Poor,” The Freeman, May 1994).

But that’s illegal, you know. In New York City, John Muney recently introduced an updated version of lodge practice: the AMG Medical Group, which for a monthly premium of $79 and a flat office fee of $10 per visit provides a wide range of services (limited to what its own practitioners can perform in-house). But because AMG is a fixed-rate plan and doesn’t charge more for “unplanned procedures,” the New York Department of Insurance considers it an unlicensed insurance policy. Muney may agree, unwillingly, to a settlement arranged by his lawyer in which he charges more for unplanned procedures like treatment for a sudden ear infection. So the State is forcing a modern-day lodge practitioner to charge more, thereby keeping the medical and insurance cartels happy—all in the name of “protecting the public.” How’s that for irony?

Regarding expensive machinery, I wonder how much of the cost is embedded rent on patents or regulatorily mandated overhead. I’ll bet if you removed all the legal barriers that prevent a bunch of open-source hardware hackers from reverse-engineering a homebrew version of it, you could get an MRI machine with a twentyfold reduction in cost. I know that’s the case in an area I’m more familiar with: micromanufacturing technology. For example, the RepRap—a homebrew, open-source 3-D printer—costs roughly $500 in materials to make, compared to tens of thousands for proprietary commercial versions.

More generally, the system is racked by artificial scarcity, as editor Sheldon Richman observed in an interview a few months back. For example, licensing systems limit the number of practitioners and arbitrarily impose levels of educational overhead beyond the requirements of the procedures actually being performed.

Libertarians sometimes—and rightly—use “grocery insurance” as an analogy to explain medical price inflation: If there were such a thing as grocery insurance, with low deductibles, to provide third-party payments at the checkout register, people would be buying a lot more rib-eye and porterhouse steaks and a lot less hamburger.

The problem is we’ve got a regulatory system that outlaws hamburger and compels you to buy porterhouse if you’re going to buy anything at all. It’s a multiple-tier finance system with one tier of service. Dental hygienists can’t set up independent teeth-cleaning practices in most states, and nurse-practitioners are required to operate under a physician’s “supervision” (when he’s out golfing). No matter how simple and straightforward the procedure, you can’t hire someone who’s adequately trained just to perform the service you need; you’ve got to pay amortization on a full med school education and residency.

Drug patents have the same effect, increasing the cost per pill by up to 2,000 percent. They also have a perverse effect on drug development, diverting R&D money primarily into developing “me, too” drugs that tweak the formulas of drugs whose patents are about to expire just enough to allow repatenting. Drug-company propaganda about high R&D costs, as a justification for patents to recoup capital outlays, is highly misleading. A major part of the basic research for identifying therapeutic pathways is done in small biotech startups, or at taxpayer expense in university laboratories, and then bought up by big drug companies. The main expense of the drug companies is the FDA-imposed testing regimen—and most of that is not to test the version actually marketed, but to secure patent lockdown on other possible variants of the marketed version. In other words, gaming the patent system grossly inflates R&D spending.

The prescription medicine system, along with state licensing of pharmacists and Drug Enforcement Administration licensing of pharmacies, is another severe restraint on competition. At the local natural-foods cooperative I can buy foods in bulk, at a generic commodity price; even organic flour, sugar, and other items are usually cheaper than the name-brand conventional equivalent at the supermarket. Such food cooperatives have their origins in the food-buying clubs of the 1970s, which applied the principle of bulk purchasing. The pharmaceutical licensing system obviously prohibits such bulk purchasing (unless you can get a licensed pharmacist to cooperate).

I work with a nurse from a farming background who frequently buys veterinary-grade drugs to treat her family for common illnesses without paying either Big Pharma’s markup or the price of an office visit. Veterinary supply catalogs are also quite popular in the homesteading and survivalist movements, as I understand. Two years ago I had a bad case of poison ivy and made an expensive office visit to get a prescription for prednisone. The next year the poison ivy came back; I’d been weeding the same area on the edge of my garden and had exactly the same symptoms as before. But the doctor’s office refused to give me a new prescription without my first coming in for an office visit, at full price—for my own safety, of course. So I ordered prednisone from a foreign online pharmacy and got enough of the drug for half a dozen bouts of poison ivy—all for less money than that office visit would have cost me.

Of course people who resort to these kinds of measures are putting themselves at serious risk of harassment from law enforcement. But until 1914, as Sheldon Richman pointed out (“The Right to Self-Treatment,” Freedom Daily, January 1995), “adult citizens could enter a pharmacy and buy any drug they wished, from headache powders to opium.”

The main impetus to creating the licensing systems on which artificial scarcity depends came from the medical profession early in the twentieth century. As described by Richman:

Accreditation of medical schools regulated how many doctors would graduate each year. Licensing similarly metered the number of practitioners and prohibited competitors, such as nurses and paramedics, from performing services they were perfectly capable of performing. Finally, prescription laws guaranteed that people would have to see a doctor to obtain medicines they had previously been able to get on their own.

The medical licensing cartels were also the primary force behind the move to shut down lodge practice, mentioned above.

In the case of all these forms of artificial scarcity, the government creates a “honey pot” by making some forms of practice artificially lucrative. It’s only natural, under those circumstances, that health care business models gravitate to where the money is.

Health care is a classic example of what Ivan Illich, in Tools for Conviviality, called a “radical monopoly.” State-sponsored crowding out makes other, cheaper (but often more appropriate) forms of treatment less usable, and renders cheaper (but adequate) treatments artificially scarce. Artificially centralized, high-tech, and skill-intensive ways of doing things make it harder for ordinary people to translate their skills and knowledge into use-value. The State’s regulations put an artificial floor beneath overhead cost, so that there’s a markup of several hundred percent to do anything; decent, comfortable poverty becomes impossible.

A good analogy is subsidies to freeways and urban sprawl, which make our feet less usable and raise living expenses by enforcing artificial dependence on cars. Local building codes primarily reflect the influence of building contractors, so competition from low-cost unconventional techniques (T-slot and other modular designs, vernacular materials like bales and papercrete, and so on) is artificially locked out of the market. Charles Johnson described the way governments erect barriers to people meeting their own needs and make comfortable subsistence artificially costly, in the specific case of homelessness, in “Scratching By: How the Government Creates Poverty as We Know It” (The Freeman, December 2007).

The major proposals for health care “reform” that went before Congress would do little or nothing to address the institutional sources of high cost. As Jesse Walker argued at Reason.com, a 100 percent single-payer system, far from being a “radical” solution,

would still accept the institutional premises of the present medical system. Consider the typical American health care transaction. On one side of the exchange you’ll have one of an artificially limited number of providers, many of them concentrated in those enormous, faceless institutions called hospitals. On the other side, making the purchase, is not a patient but one of those enormous, faceless institutions called insurers. The insurers, some of which are actual arms of the government and some of which merely owe their customers to the government’s tax incentives and shape their coverage to fit the government’s mandates, are expected to pay all or a share of even routine medical expenses. The result is higher costs, less competition, less transparency, and, in general, a system where the consumer gets about as much autonomy and respect as the stethoscope. Radical reform would restore power to the patient. Instead, the issue on the table is whether the behemoths we answer to will be purely public or public-private partnerships. [“Obama is No Radical,” September 30, 2009]

I’m a strong advocate of cooperative models of health care finance, like the Ithaca Health Alliance (created by the same people, including Paul Glover, who created the Ithaca Hours local currency system), or the friendly societies and mutuals of the nineteenth century described by writers like Pyotr Kropotkin and E. P. Thompson. But far more important than reforming finance is reforming the way delivery of service is organized.

Consider the libertarian alternatives that might exist. A neighborhood cooperative clinic might keep a doctor of family medicine or a nurse practitioner on retainer, along the lines of the lodge-practice system. The doctor might have his med school debt and his malpractice premiums assumed by the clinic in return for accepting a reasonable upper middle-class salary.

As an alternative to arbitrarily inflated educational mandates, on the other hand, there might be many competing tiers of professional training depending on the patient’s needs and ability to pay. There might be a free-market equivalent of the Chinese “barefoot doctors.” Such practitioners might attend school for a year and learn enough to identify and treat common infectious diseases, simple traumas, and so on. For example, the “barefoot doctor” at the neighborhood cooperative clinic might listen to your chest, do a sputum culture, and give you a round of Zithro for your pneumonia; he might stitch up a laceration or set a simple fracture. His training would include recognizing cases that were clearly beyond his competence and calling in a doctor for backup when necessary. He might provide most services at the cooperative clinic, with several clinics keeping a common M.D. on retainer for more serious cases. He would be certified by a professional association or guild of his choice, chosen from among competing guilds based on its market reputation for enforcing high standards. (That’s how competing kosher certification bodies work today, without any government-defined standards). Such voluntary licensing bodies, unlike state licensing boards, would face competition—and hence, unlike state boards, would have a strong market incentive to police their memberships in order to maintain a reputation for quality.

The clinic would use generic medicines (of course, since that’s all that would exist in a free market). Since local juries or arbitration bodies would likely take a much more common-sense view of the standards for reasonable care, there would be far less pressure for expensive CYA testing and far lower malpractice premiums.

Basic care could be financed by monthly membership dues, with additional catastrophic-care insurance (cheap and with a high deductible) available to those who wanted it. The monthly dues might be as cheap as or even cheaper than Dr. Muney’s. It would be a no-frills, bare-bones system, true enough—but to the 40 million or so people who are currently uninsured, it would be a pretty damned good deal.

#health care#monopoly#us healthcare#us politics#healthcare#medicine#science#kevin karson#anarchism#anarchy#anarchist society#practical anarchy#practical anarchism#resistance#autonomy#revolution#communism#anti capitalist#anti capitalism#late stage capitalism#daily posts#libraries#leftism#social issues#anarchy works#anarchist library#survival#freedom

2 notes

·

View notes

Text

0 notes

Text

Hospitals and Ambulatory Surgery Centers in Washington DC: A Comprehensive Guide

Why Washington DC is a Hub for Quality Healthcare

The capital city is renowned for its cutting-edge healthcare institutions, attracting patients from across the country. Washington DC’s hospitals and ASCs prioritize patient-centered care, advanced technology, and highly skilled medical professionals. The city’s healthcare facilities also cater to a variety of specialties, including cardiology, orthopedics, oncology, and pediatrics.

Ambulatory Surgery Centers: A Growing Trend

Ambulatory Surgery Centers are transforming healthcare in Washington DC by offering high-quality surgical care in an outpatient setting. ASCs are designed for efficiency, often providing same-day procedures with quicker recovery times compared to traditional hospital settings.

Benefits of ASCs in Washington DC:

· Convenience: Shorter wait times and easy scheduling.

· Cost-Effectiveness: Lower costs compared to hospital surgeries.

· Specialized Care: Focused expertise in areas like orthopedics, gastroenterology, and ENT.

Key Features of ASCs:

Efficiency: Streamlined processes reduce wait times and improve scheduling flexibility.

Cost Savings: Procedures at ASCs are often more affordable than those performed in hospital settings.

Specialized Care: ASCs frequently concentrate on specific types of surgeries, such as orthopedic, gastrointestinal, or cosmetic procedures.

For individuals with non-emergency medical needs, ASCs provide a practical and convenient option.

Choosing Between Hospitals and ASCs

When deciding between a hospital and an ASC in Washington DC, consider the complexity of the procedure, your health insurance coverage, and the recommendations of your healthcare provider. Hospitals are better suited for complex surgeries and emergency care, while ASCs are ideal for planned, minimally invasive procedures.

Choosing the Right Facility

Selecting between a hospital and an ambulatory surgery center depends on several factors:

Procedure Complexity: Hospitals are better suited for high-risk or intricate surgeries, while ASCs handle routine, minimally invasive procedures.

Health Insurance Coverage: Verify whether your insurance plan covers the facility and procedure.

Recovery Requirements: If extended monitoring or overnight care is needed, a hospital may be the better choice.

Personal Preferences: Some patients prioritize shorter visits and the convenience of ASCs, while others value the comprehensive services of a hospital.

The Future of Healthcare in Washington DC

As Washington DC continues to evolve as a healthcare hub, hospitals and ASCs are adopting innovative practices to improve patient outcomes. From telemedicine integration to advanced robotic surgeries, the city remains at the forefront of medical advancements.

Conclusion

Whether you need comprehensive care at a hospital or a convenient outpatient procedure at an ambulatory surgery center, Washington DC offers a wealth of options to meet your healthcare needs. By choosing the right facility, you can ensure high-quality care tailored to your condition.

Explore your options today and experience the best Hospitals and Ambulatory Surgery Center in Washington DC.

0 notes

Text

Choosing the Right Primary Care Las Vegas Facility

Like education, selecting a qualified and qualified primary care doctor is one of life’s most important decisions related to health care. Picking a suitable PCP in a quickly growing city such as LV with a multicultural population base and a range of healthcare centers is challenging. You are a newcomer or a patient who is not happy with your current panel physician; it is important to know how to assess and make a correct decision. In this guide, you will discover what to look for when choosing a primary care Las Vegas center and its provider.

What is Primary Care?

Now that we know what primary care means it is possible to proceed to explain how one can go about choosing the right primary care facility. Main care is the routine care that treats the common health issues of persons. Your PCP will be responsible for both routine and sick care, preventive services, disease and illness, and connecting with other specialists if appropriate. The services profiled here are available at solo practitioners’ offices in Las Vegas and large multispecialty centers.

Consider the Type of Primary Care Facility

Las Vegas has many primary care facilities and it is crucial to know the differences between the types to determine what will be best for you. Some of the most common types include:

Private Practice: Free-standing facilities staffed by one or several physicians or a group of physicians practicing independently of a hospital. These are usually preferred due to Individualized attention and proximity of the doctor-patient intimacy.

Urgent Care Centers: These are centers for the first treatment of ambulatory patients who have injuries or diseases that are not critical. They are not a substitute for primary care physicians but can be used when we require convenient urgent care.

Multi-Specialty Clinics: Large health organizations that provide primary care, specialization care, diagnostic services, and surgeries are the second category of health facilities. These clinics may suitcases where the patient has one or more health complications that need attention.

Community Health Centers: It is strongly suggested that most of these centers receive public support and are expected to serve needy populations. While they are quite cheap, they may always be unavailable when needed or clients may have to wait longer for a provider.

Accessibility and Convenience

In a place like Vegas, it makes a lot of sense to select your main doctor based on convenience. The center should be located close to your home or place of work for convenience about transportation. Consider the following factors to make sure the location is suitable:

Proximity: Select a primary care Las Vegas facility that you can probably visit easily within the shortest time possible. If you are partially mobile or busy, the clinic nearby would prove to be much more convenient for you.

Office Hours: Some of the providers may be willing to have extended business hours, or even availability on weekends to attend to patients that have tight working schedules. Be sure to find a healthcare facility that has working hours that can be agreed on and are convenient.

Appointment Availability: A good primary care office should provide appointments with minimal wait time. Learn how much time it takes to schedule an appointment because this can take a long time in some companies.

Evaluating the Quality of Care

When it comes to the selection of an appropriate primary care Las Vegas facility, the focus has to be made on the quality of care that clients will be featured with. Here are some key factors to evaluate:

Qualifications of Providers: Ensure that whoever the facility has in doctors, either a doctor, nurse practitioner, or physician assistant is board-certified and qualified. One can visit hospitals and orthopedic doctors with the recommendations of other patients to determine the quality of care.

Specializations and Services: Many PCP have their concentrate on comprehensive areas that include family, pediatric, geriatric, or internal medicine. Based on the kind of health facilities and specific health needs you want, then you should look for a health facility that provides the sort of care you need.

Patient Reviews: With the modern technologies available, information about other patients’ experiences can be obtained from online sources. Today there are such web platforms as Google, Yelp, and Healthgrades that let patients share their impressions about a particular facility. It is also preferable to focus on both good and bad accounts to compare them with each other.

Communication Style: One should have a good rapport with one's direct care provider or the primary health care physician. When going to see a doctor or a healthcare provider, consider how effectively they speak to you. Can they take your calls and be receptive to what you have to say including answering your questions? That way, do they provide you with such feelings that you are valued and respected as a patient?

Insurance and Affordability

It is to be noted that the price of the services will depend on the insurance company and the particular primary care Las Vegas center that is selected. First, you must ensure that the selected primary care provider takes your insurance plan before setting your appointment. If someone does not have insurance ask about the possibility of self-payment, and always know exactly how much the service will be.

Further, some facilities may be charging on an affordable scale or they may be willing to accept installments for the payment they’re offering which makes it easier for those with scarce cash to access affordable healthcare. To make necessary changes or switch providers compare different providers in your area by price and type of service they offer for the best value for your money.

Building a Long-Term Relationship

Here it’s crucial to find a primary care provider with whom the patient will be working in years to come, therefore, finding a personality that will complement the patient’s is critical to building that healthy provider-patient relationship. Frequent contact with your Star/Primary Care Provider is beneficial because you become their patient, and they become more knowledgeable about your health.

Conclusion

Finding the right primary care center in Las Vegas is a crucial decision toward improved well-being. When it comes to the choice between a private clinic, and a large facility, multi-specialty considerations can be very important although the most important factors to take into account are the location and accessibility of the clinic and, therefore, the quality of care offered. By analyzing things like location, the health care provider, the patients’ ratings, the insurance companies accepted and the general quality, it’s possible to avoid making the wrong decision on a health care provider and get the best care possible. Be patient and make sure the doctor not only hears you when you talk about your health. Share the fact that you are still looking for first client as you stated your health is invaluable and do not rush the process.

0 notes

Text

RCM Outsourcing for Hospitals: Streamlining Complex Billing and Coding This blog will explore how outsourcing revenue cycle management can help hospitals handle complex billing and coding challenges, streamline processes, and ensure accurate claims submissions for faster reimbursement.

How RCM Outsourcing Supports Healthcare Organizations in Value-Based Reimbursement Models With the shift towards value-based care, accurate billing and reimbursement are more important than ever. This blog will discuss how RCM outsourcing supports healthcare organizations in transitioning to and managing value-based reimbursement models.

The Benefits of RCM Outsourcing for Ambulatory Surgical Centers (ASCs) Ambulatory surgical centers (ASCs) have unique revenue cycle management needs due to the nature of their services. This blog will explore how outsourcing RCM can help ASCs streamline billing, ensure compliance, and improve cash flow.

How RCM Outsourcing Improves Insurance Verification and Authorization Insurance verification and authorization are critical to ensuring timely reimbursement for healthcare services. This blog will discuss how outsourcing RCM can improve the accuracy and speed of insurance verification and authorization processes.

The Role of RCM Outsourcing in Reducing Healthcare Fraud and Abuse Fraud and abuse can significantly impact the financial health of healthcare organizations. This blog will focus on how RCM outsourcing helps detect and prevent fraudulent activities, ensuring compliance and reducing financial losses.

RCM Outsourcing for Long-Term Care Providers: Managing Complex Billing Needs Long-term care providers face unique billing challenges due to the variety of services provided and patient needs. This blog will explore how outsourcing RCM can help long-term care providers streamline their billing processes, improve collections, and reduce administrative burdens.

How RCM Outsourcing Helps Healthcare Providers Navigate the ICD-10 Transition The transition to ICD-10 coding presented challenges for many healthcare providers. This blog will discuss how RCM outsourcing can ease the transition by providing expert support in coding and ensuring compliance with the new system.

Reducing Denials with RCM Outsourcing: Best Practices and Strategies Denials are a major roadblock in revenue cycle management. This blog will provide best practices and strategies for reducing denials through RCM outsourcing, including improving claim accuracy and addressing common causes of denials.

How RCM Outsourcing Drives Operational Efficiency in Healthcare Practices Operational efficiency is critical for the financial success of healthcare organizations. This blog will explore how outsourcing RCM can improve operational efficiency by automating processes, reducing administrative workload, and accelerating reimbursement timelines.

Why RCM Outsourcing is a Smart Choice for Rural Healthcare Providers Rural healthcare providers often struggle with limited resources and high administrative burdens. This blog will highlight how RCM outsourcing can help rural providers manage their revenue cycles more effectively, improve cash flow, and reduce operational strain.

The Impact of RCM Outsourcing on Healthcare Payer-Provider Relationships Effective communication between payers and providers is essential for efficient reimbursement. This blog will examine how RCM outsourcing helps improve payer-provider relationships, reduce disputes, and ensure smoother claims processing.

RCM Outsourcing for Mental Health and Addiction Treatment Centers Mental health and addiction treatment centers face unique challenges in billing and reimbursement. This blog will discuss how outsourcing RCM can help these centers manage claims, ensure compliance, and reduce administrative overhead.

The Evolution of RCM Outsourcing: Trends in Technology and Service Delivery RCM outsourcing is constantly evolving. This blog will explore current trends in the field, such as the use of artificial intelligence, robotic process automation (RPA), and machine learning, and how these technologies are transforming service delivery.

How RCM Outsourcing Reduces Billing Errors and Improves Claim Accuracy Billing errors can lead to lost revenue and delayed payments. This blog will highlight how outsourcing RCM helps reduce billing errors and ensures that claims are submitted accurately, leading to faster reimbursement and improved cash flow.

Integrating RCM Outsourcing with Healthcare CRM Systems for Better Patient Management Customer relationship management (CRM) systems are crucial for managing patient interactions and improving care. This blog will explore how integrating RCM outsourcing with CRM systems can enhance both financial and patient management processes.

The Role of RCM Outsourcing in Healthcare Cost Containment Healthcare organizations are under constant pressure to reduce costs. This blog will discuss how outsourcing RCM can help contain costs by improving billing efficiency, reducing administrative overhead, and ensuring more timely reimbursements.

RCM Outsourcing for Pediatric Practices: Managing the Complexities of Pediatric Billing Pediatric practices face unique billing challenges due to insurance coverage nuances, varying reimbursement rates, and diverse services. This blog will explore how outsourcing RCM can help pediatric practices navigate these complexities while ensuring faster and more accurate reimbursement.

Why Collaboration is Key in RCM Outsourcing Partnerships Successful RCM outsourcing requires strong collaboration between healthcare providers and their outsourcing partners. This blog will discuss how fostering a collaborative relationship leads to better outcomes, such as improved collections and reduced denials.

How RCM Outsourcing Can Help Providers Navigate the Shift to Telehealth The rapid growth of telehealth has created new challenges for revenue cycle management. This blog will explore how RCM outsourcing can help healthcare providers navigate the complexities of telehealth billing and reimbursement, ensuring timely and accurate payments.

How RCM Outsourcing Helps Healthcare Providers Improve Financial Forecasting Accurate financial forecasting is essential for healthcare providers to maintain stability. This blog will discuss how RCM outsourcing can provide data and insights to improve financial forecasting and help healthcare organizations plan for the future.

The Future of RCM Outsourcing: Key Challenges and Opportunities As the healthcare landscape continues to evolve, RCM outsourcing must adapt. This blog will explore key challenges that the RCM outsourcing industry will face in the future and the opportunities these challenges present for both providers and outsourcing partners.

How RCM Outsourcing Can Support Healthcare Mergers and Acquisitions Mergers and acquisitions in healthcare often lead to complex billing and reimbursement challenges. This blog will discuss how RCM outsourcing can support organizations during mergers and acquisitions by streamlining billing, improving consistency, and reducing operational disruption.

0 notes